5 Takeaways from the Inflation + Energy War Room

It’s been a volatile couple of months for the market. As we discussed in January’s War Room, inflation remains a concern–one that will shape Fed policy in the coming months.

But what about energy? While the negative crude oil prices of early 2020 are now a distant memory, the specter of inflation looms and leaves many questioning the effect it may have on the energy markets.

Add to the mix the developing situation with the Russian attack on Ukraine. Russia is the number two producer of oil globally–behind the U.S.–and between sanctions and stalled pipelines, we’re starting to see the conflict’s effects on global energy supply and pricing.

It was in this tumultuous reality that we hosted February’s War Room on inflation and energy. While the situation will remain a moving target in the coming weeks and months, some takeaways can guide investors through it all.

1. “Sell the rumor, buy the news” on Russia and Ukraine.

With the developing conflict on Ukrainian soil, we saw the opposite of the old market truism, “Buy the rumor, sell the news.”

As Russian President Vladimir Putin began his attack on Ukraine on Thursday, February 24, markets initially faltered. By Friday, U.S. markets were charging upward.

Investors were skittish in the days and weeks leading up to the first attack. The constant drumbeat of threats from Putin put observers on edge. When the threats came to fruition, it seemed to–perhaps counterintuitively–tame some of the market volatility.

2. Bright skies are ahead for the companies that can weather inflation.

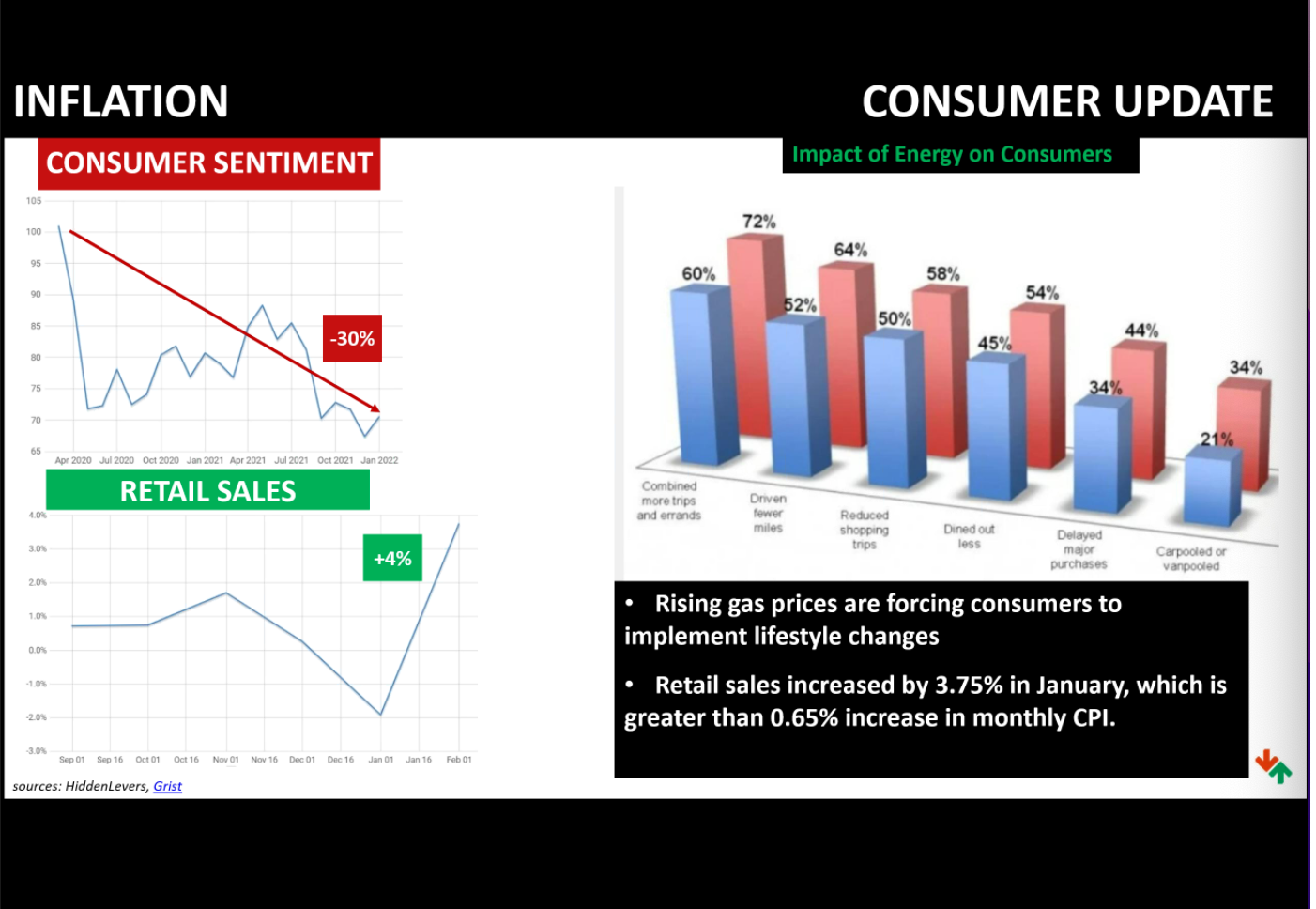

With CPI at 7.5%, there’s no question that inflation remains a concern. But earnings are on the rise, too.

That’s because consumers are continuing to spend. After months cooped up in 2020–with nowhere to go and nothing to buy–it seems folks are ready to go out and splurge with some of the money they saved up during the early pandemic.

Retail sales were up nearly 4% in January, a rate that vastly outpaces the .65% increase in monthly CPI. That means companies are still coming out ahead, despite inflationary pressures.

The organizations that can push through this period of inflation will find themselves poised for growth.

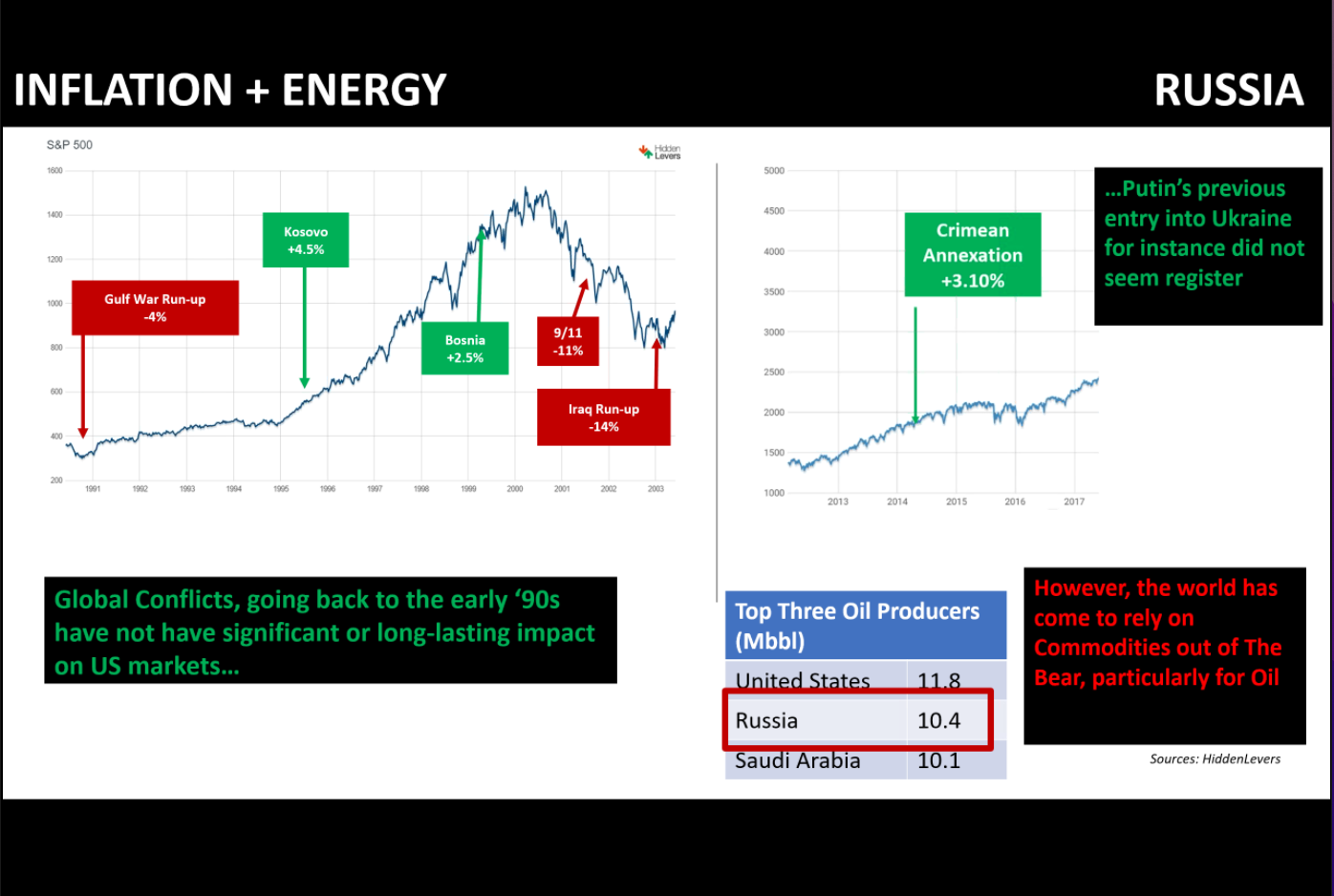

3. Wars abroad don’t often impact U.S. markets.

Russia’s attack on Ukraine certainly has devastating geopolitical and humanitarian implications. But when it comes to U.S. markets, the influence of overseas wars has historically been minimal.

For example, the previous instance of Russian aggression against Ukraine–the annexation of Crimea in 2014–did not have an impact on markets here.

4. The Fed cannot fix secular inflation.

When it comes to taming high inflation rates, the Fed’s toolbox is limited. While it can slow quantitative easing, reduce its balance sheet, and hike rates, this only addresses the demand side.

However, much of the inflation we’re currently seeing is on the supply side. The costs of food, energy, vehicles, and shelter are not something the Fed can directly address or adjust.

Therefore, we may continue to see inflation rise even if the Fed takes a hawkish approach.

5. The good, baseline, and ugly.

So, where does this all leave our portfolios?

While it’s not possible to foretell exactly what the future holds, our Inflation + Energy scenario can help advisors see how this might play out and the impact it will have on clients’ investments.

In a best-case scenario, earnings keep growing despite inflation. Consumers continue to tap into reserves they saved during the pandemic, and spending remains high even if inflation doesn’t slow down.

In a baseline scenario, we see the limitations of the Fed’s impact on secular inflation play out in the markets. Supply/demand remains off-kilter, and oil prices rise as a result.

Finally, there’s the ugly scenario. In this world, the wage increases we’re already seeing take a greater toll on employers. During the pandemic, millions of Americans opted to retire early. And with immigration rates slowed, too, there are simply fewer people to fill open positions.

That puts pressure on employers to pay higher wages. As the cost of doing business continues to rise, we may eventually hit a breaking point.

If there’s one thing we’ve seen illustrated over the past week, it’s that scenarios can change quickly. That’s why HiddenLevers is constantly updating its online scenario library. Keep checking in for updates to our Inflation + Energy and Russia Invasion scenarios.

Learn how the dynamic fintech combination of HiddenLevers and ORION can help you better serve your clients.

Access to the services presented is provided solely as a service to financial advisors. HiddenLevers does not make recommendations or determine the suitability of any security or strategy. Past performance of a security or strategy does not guarantee future results. HiddenLevers research and tools are provided for informational purposes only. While the information is deemed reliable, HiddenLevers does not guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with respect to the results to be obtained from its use.

0445-OAT-3/14/2022